Asset disposition is defined as the formal process of removing property from a company’s financial records and physical control once it no longer provides economic value. The term covers a broad range of actions, from selling a manufacturing line to scrapping obsolete equipment or donating surplus inventory. Understanding the asset disposition definition matters because each method carries distinct accounting, tax, and legal consequences. Asset managers who treat disposition as a routine accounting task routinely leave money on the table and expose their organizations to compliance risk.

Asset disposition is the formal process of removing property from a company’s financial records and control when it no longer provides economic value. That definition sounds simple, but the execution involves three coordinated disciplines: accounting, legal transfer, and physical removal. Each discipline must close out cleanly before the asset is truly gone from the books.

The accounting dimension requires removing the asset’s original cost and accumulated depreciation from the balance sheet. The legal dimension requires transferring title or documenting destruction. The physical dimension requires confirming the asset is no longer in service. Organizations that skip any one of these steps create what practitioners call “ghost assets,” which are assets that appear on the books but no longer exist in reality.

The meaning of asset disposition also extends to regulatory compliance. The IRS requires documentation for abandonment, including photographic evidence or disposal certifications. Failing to produce that documentation can trigger penalties and force restatement of prior financial periods. Asset managers must treat disposition as a formal close-out event, not a footnote.

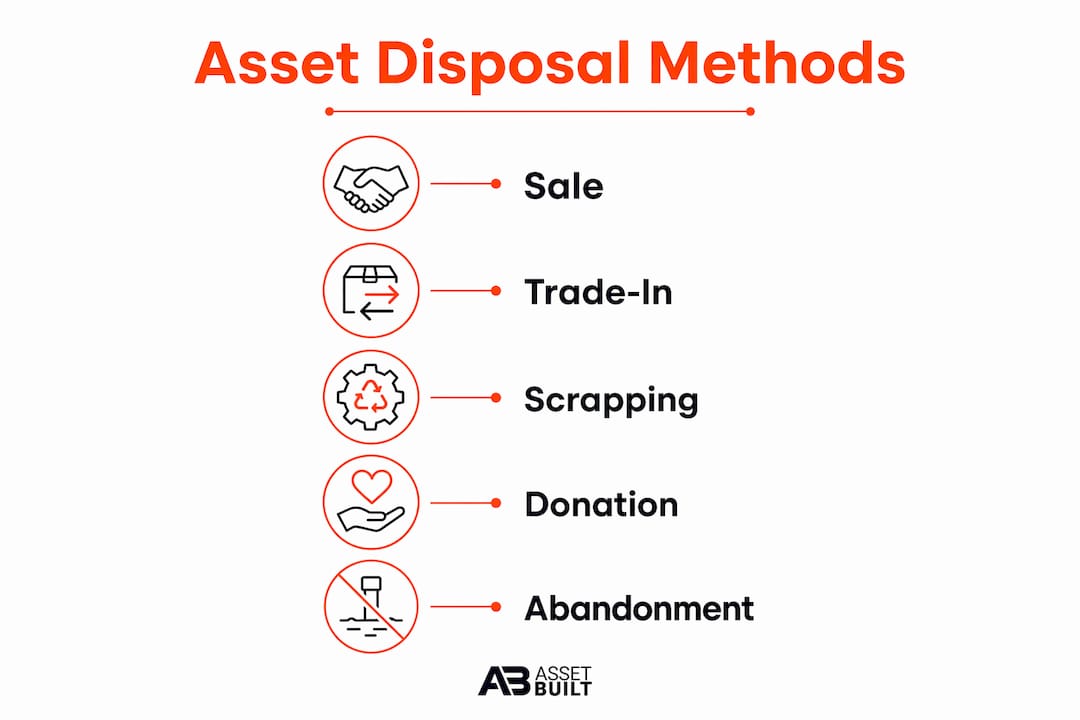

Five primary methods govern how organizations dispose of assets: sale, trade-in, scrapping, donation, and abandonment. Each method produces a different financial outcome and applies in different circumstances.

An outright sale is the most common method and the one most likely to generate a taxable gain. The seller receives cash or a note, removes the asset from the books, and records a gain or loss based on the difference between proceeds and net book value. Asset Purchase Agreements govern these transactions, and purchase price allocations are critical for determining tax exposure. Sellers must explicitly exclude environmental or legacy liabilities from the agreement to avoid inheriting future obligations.

A trade-in applies the old asset’s value as a credit toward a replacement. The accounting treatment requires recognizing any gain or loss on the surrendered asset at fair market value. Tax rules on trade-ins vary by asset class, so asset managers should confirm treatment with a tax advisor before finalizing the exchange.

Scrapping applies when an asset has no resale value. The organization removes the cost and accumulated depreciation, records any remaining net book value as a loss, and documents the physical destruction. Donation transfers the asset to a qualifying nonprofit. The donor may claim a deduction equal to the asset’s fair market value, subject to IRS substantiation rules.

Abandonment is the most documentation-intensive method. The IRS requires written evidence that the asset was permanently retired and that no proceeds were received. A loss equal to the remaining net book value is deductible, but only when the abandonment is complete and documented.

| Method | Typical trigger | Financial outcome |

|---|---|---|

| Sale | Asset has residual market value | Gain or loss on proceeds vs. book value |

| Trade-in | Replacement purchase planned | Gain or loss at fair market value |

| Scrapping | No resale value remains | Loss equal to remaining book value |

| Donation | Nonprofit transfer planned | Deduction at fair market value |

| Abandonment | Asset retired with no proceeds | Deductible loss with IRS documentation |

Proper accounting for disposition requires calculating gain or loss by subtracting the asset’s net book value from the proceeds received. Net book value equals original cost minus total accumulated depreciation. When proceeds exceed net book value, the organization records a gain. When proceeds fall short, it records a loss.

The tax calculation adds a layer of complexity through depreciation recapture. IRC Sections 1245 and 1250 govern recapture rules for personal property and real property respectively. Under Section 1245, any gain up to the amount of depreciation previously claimed is taxed as ordinary income, not as a capital gain. That distinction matters because ordinary income rates are typically higher than long-term capital gain rates.

Ghost assets inflate balance sheets and create IRS compliance risk. Many organizations fail to record final depreciation at the time of disposal, which distorts both the income statement and the tax return. That error compounds over time as the phantom asset continues to depreciate on paper.

Pro Tip: Run a physical asset verification at least once per year and reconcile the results against your fixed asset register. Any asset that cannot be physically located should trigger an immediate disposition review.

Fixed asset disposal is the most error-prone stage of the asset lifecycle. Rigorous attention to recording and legal steps prevents compliance issues that can take years to unwind.

Effective asset disposition improves liquidity, reduces maintenance costs, and frees storage space. Asset managers who treat disposition as a strategic function, not just an end-of-life accounting task, consistently recover more residual value from aging assets.

The liquidity benefit is direct. Selling or auctioning surplus equipment converts idle capital into cash that can fund operations or new investments. The maintenance benefit is equally concrete: every asset removed from the register eliminates its associated repair, insurance, and storage costs. For large industrial portfolios, those savings accumulate quickly.

Disposition is often misunderstood as mere accounting closure, but it critically affects operational efficiency and cash flow. Organizations that build formal disposition programs into their asset management strategies recover value that informal processes leave behind.

Accurate asset records also support regulatory compliance. Auditors and lenders rely on balance sheet data to assess financial health. Ghost assets and unrecorded disposals distort that picture and can trigger audit findings or covenant violations. A clean fixed asset register is a direct output of disciplined disposition practice.

Proper disposition involves three main phases: physical removal, legal transfer, and accounting cleanup. Some organizations add data security as a critical fourth phase, particularly when disposing of IT equipment or assets containing sensitive information.

Authorization is the starting point for every disposition. No asset should leave the register without a signed disposal form, management approval, and, for significant transactions, a formal board resolution. Board-level oversight is necessary for major asset dispositions to protect fiduciary duties and avoid personal liabilities for management. Formal resolutions are standard for significant sales, especially of real estate or operating units.

Pro Tip: For IT asset dispositions, require a certificate of data destruction from a certified vendor before closing the accounting entry. That certificate is your defense against data breach liability.

Misapplication of depreciation recapture rules leads to costly tax miscalculations. Businesses must verify the adjusted basis of every asset before reporting a gain or loss on disposition.

Asset disposition is a formal, multi-phase process that requires coordinated accounting, legal, and physical steps to recover value, maintain compliance, and keep financial records accurate.

| Point | Details |

|---|---|

| Formal definition | Asset disposition removes property from financial records when it no longer provides economic value. |

| Five core methods | Sale, trade-in, scrapping, donation, and abandonment each carry distinct tax and accounting outcomes. |

| Ghost asset risk | Failing to record disposals inflates balance sheets and creates IRS compliance exposure. |

| Depreciation recapture | IRC Sections 1245 and 1250 can convert capital gains into ordinary income, raising the tax cost. |

| Board oversight required | Major dispositions, especially real estate and operating unit sales, require formal board resolutions. |

After years of working through complex industrial and real estate transactions, the pattern I see most often is this: organizations treat asset disposition as a back-office task until something goes wrong. A ghost asset surfaces during an audit. A tax return gets restated because depreciation recapture was miscalculated. A former employee’s laptop turns up in a secondary market with company data still on it.

The organizations that avoid those outcomes share one habit. They build disposition into their asset management strategies from the moment an asset is acquired, not after it has already become a problem. They assign ownership, set review triggers, and maintain documentation standards that hold up under IRS scrutiny.

The uncomfortable truth about asset disposition is that the financial upside is often larger than managers expect. Surplus industrial equipment, real estate, and operating assets frequently carry recoverable value that informal disposal processes destroy. A structured auction or private treaty sale, executed with proper legal and accounting support, routinely outperforms a rushed internal write-off.

Proactive disposition planning is not a finance department luxury. It is a core function of sound asset lifecycle management, and the organizations that treat it that way consistently outperform those that do not.

— Jake Freedlander

Assetbuilt operates across the full asset disposition lifecycle, from initial advisory and capital alignment through final execution. Whether the transaction involves industrial equipment, real estate, or an operating business, Assetbuilt brings execution-focused expertise to every phase.

Assetbuilt’s capital services are structured to recover maximum residual value from surplus and end-of-life assets. The firm’s business advisory team helps asset managers build disposition programs that align with broader financial and operational objectives. For organizations with immediate liquidation needs, Assetbuilt’s industrial equipment auctions provide a proven channel for converting surplus assets into capital efficiently and transparently.

Asset disposition is the formal removal of an asset from a company’s financial records and physical control once it no longer provides economic value. The process requires removing the asset’s cost and accumulated depreciation from the balance sheet and recording any resulting gain or loss.

The five primary methods are sale, trade-in, scrapping, donation, and abandonment. Each method produces different tax and accounting outcomes depending on the asset’s condition and the proceeds received.

Depreciation recapture requires a portion of the gain on asset sale to be taxed as ordinary income rather than as a capital gain, under IRC Sections 1245 and 1250. This increases the effective tax cost of disposing of fully or partially depreciated assets.

A ghost asset is an item that remains on the fixed asset register after it has been physically removed or destroyed. Ghost assets inflate balance sheets, distort depreciation expense, and create IRS compliance risk if not corrected.

Major dispositions, particularly sales of real estate or operating units, require formal board resolutions to satisfy fiduciary duties and protect management from personal liability. Routine disposals of low-value assets typically require only management-level authorization.